“A good plan violently

executed now is better than a perfect plan next week."

General George S. Patton

General George S. Patton

A DETAILED PLAN BEFORE EVERY TRADE

Develop a plan before

every trade. Include an exit strategy. Decide before you take a position where

you will exit if the trade goes against you. Let me repeat this point. Before

you make a trade, have an exit plan for where you will exit a stock (or ETF or

other product) if it goes against you. This is the single most important aspect

of trading. Again, know where you will exit your trade if it goes against you.

Never take a position without an exit plan.

Your plan should also

include an exit strategy if the stock trades in your favor. What will make you

sell the stock or other product? Will you sell the stock if it trades at a

certain price? Will you sell it after a substantial up move or when a large

seller appears? The details of the plan are important, but actually having a

plan is most important.

Here is an example of a

plan…….

I notice that NYSE is

offering stock at 30, and this is an important intraday resistance level. If

NYSE lifts, I will buy the stock and hold until either the offer is 29.90 or

the stock trades at 30.50. I will also consider selling if a new large seller

appears before 30.50.

Learn to develop detailed

plans.

Let's take the same plan

from above and make it more detailed. I notice that NYSE is selling at 30. If

NYSE lifts, I will buy the stock and hold until either the offer is 29.90 or

the stock trades at 30.50. I will also consider selling if a new large seller

appears before 30.50. If NYSE lifts 30 and the futures begin to rapidly

decline, I will consider selling the stock.

And now even more

detailed....if NYSE lifts 30 and the futures quickly worsen, I will consider

selling the stock if I notice weakness on the tape.

SUMMARY

1) Develop a detailed

plan for every trade.

2) Develop an exit plan.

3) Develop an exit plan

if the stock goes against you and if it trades in your favor.

The importance of an exit

plan is magnified by the story that follows concerning the fall of Amaranth and

the losses sustained by a “great trader”, who had no exit plan.

Blue Flameout

How Giant Bets on Natural Gas Sank Brash Hedge-Fund Trade

Up in Summer, Brian Hunter Lost $5 Billion in a Week As Market Turned on Him A Low-Profile Life in Calgary By ANN DAVIS September 19, 2006; Page A1

How Giant Bets on Natural Gas Sank Brash Hedge-Fund Trade

Up in Summer, Brian Hunter Lost $5 Billion in a Week As Market Turned on Him A Low-Profile Life in Calgary By ANN DAVIS September 19, 2006; Page A1

CALGARY, Alberta -- Of

all the traders gambling big sums on energy, a 32-year-old Canadian named Brian

Hunter made some of the brashest bets and the fastest money.

Last week, he fell hard,

proof of how quickly fortunes can reverse in gyrating commodities markets.

Here in this bustling new

energy frontier, Mr. Hunter headed the energy desk for a Connecticut hedge fund

called Amaranth Advisors. At the end of August, trading natural gas, he was up

approximately $2 billion for the year. Then Mr. Hunter lost roughly $5 billion,

in about a week.

His losses savaged

returns for Amaranth, dragging its assets under management down to $4.5 billion

from $9 billion at the start of September. In disclosing the losses to

investors in a letter yesterday, the fund said it was "aggressively

reducing" its natural-gas bets, though Mr. Hunter remains at the fund.

(Even as Amaranth was losing, some gas traders were winning; see article1.)

What hurt Mr. Hunter is

what he had ridden to glory for the past year or so: volatility.

Though unknown in public,

he had created a buzz on Wall Street -- a wunderkind to some, a ticking bomb to

others. From a cramped trading desk here, he thrived on big price swings,

reaping billions of dollars on price declines and surges alike. But late last

week, he watched with growing alarm as gas prices took a steep dive,

particularly in futures contracts for delivery of gas for this coming winter.

His losses mounted in afterhours trading last weekend.

"The cycles that

play out in the oil market can take several years, whereas in natural gas,

cycles take several months," Mr. Hunter said in an interview late in July,

when his returns were looking rosy. "Every time you think you know what

these markets can do, something else happens."

At that time, Mr. Hunter

had more than $3 billion of bets outstanding, investors familiar with the

funds' holdings say. Soon thereafter, a heat wave caused gas prices to go

haywire, then soar. Many traders took hits. One energy-trading firm, MotherRock

L.P. in New York, imploded and decided to close shop. The lanky Mr. Hunter,

however, came out hundreds of million of dollars ahead in August, Amaranth

investors say, and continued taking positions some other traders had abandoned

as too risky. He declined to be interviewed yesterday.

An increasing number of

big commodity players are bypassing the geopolitics of oil for the most-volatile

major commodity: natural gas. The blue-burning fuel heats 52% of U.S. homes and

runs many power plants in peak air-conditioning season. It also is a raw

material in industries from fertilizers to chemicals.

WALL STREET JOURNAL

WSJ's Greg Zuckerman comments on the risk in betting on natural gas and the overall energy markets.

WSJ's Greg Zuckerman comments on the risk in betting on natural gas and the overall energy markets.

Unlike oil, gas can't

readily be moved about the globe to fill local shortages or relieve local

surpluses. Forecasts of freezing U.S. temperatures in winter or heat and

hurricanes in summer can send prices jumping, while forecasts of mild weather

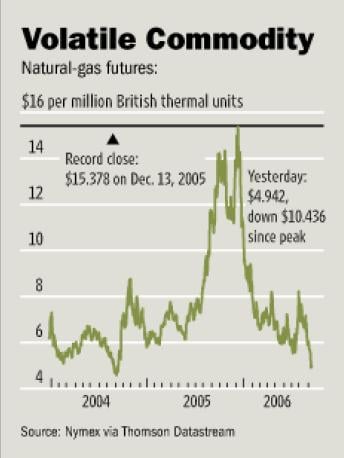

can do the opposite. Last December, amid a cold snap, gas soared to a record

$15.378 a million British thermal units on the New York Mercantile Exchange, or

Nymex. This month, prices fell below $5 in the absence of major hurricanes and

with forecasters talking about another warm winter. Yesterday, gas for October

delivery settled at $4.942 a million BTUs on Nymex, off four cents.

Backed by borrowed money

and a deep-pocketed fund, Mr. Hunter took on more exposure to certain futures

contracts than do some big investment banks employing more than 100 energy

traders, say several traders and ex-colleagues. He sometimes held open

positions to buy or sell tens of billions of dollars of commodities.

He was up for the year

roughly $2 billion by April, scoring a return of 11% to 13% that month alone,

say investors in the Amaranth fund. Then he had a loss of nearly $1 billion in

May when prices of gas for delivery far in the future suddenly collapsed, investors

add. He won back the $1 billion over the summer, only to lose that and much

more last week.

The whiplash trading in

these markets could work to the detriment of energy consumers. Some consumer

advocates, utilities and federal officials say speculation in the energy

markets accentuates the volatility of this staple fuel and that the increased

volatility, in itself, hurts consumers. Volatility makes it harder for

utilities and municipalities to determine the best time to buy gas for their

operations. Many utilities made gas purchases over the past year that proved to

be poorly timed. They passed on those costs to electricity and heating

customers, even as futures prices were dropping.

'A Typical Mistake'

While energy consumers

have seen their bills rise, many traders' paychecks have soared. Mr. Hunter is

estimated to have taken home $75 million to $100 million last year. His swift

reversal calls into question how well some hedge funds grasp the risk they are

taking in the now-popular energy markets. Vince Kaminski, a risk-management

expert who protested chancy trades while at Enron Corp. and until recently was

at Citigroup Inc.'s commodities desk, said yesterday that it is dangerous to

take giant positions in relatively shallow markets, which certain months are in

gas futures. "This is a typical mistake of inexperienced and aggressive

traders," he said. Mr. Hunter "appeared to have a position that the

entire market knew about. The markets are very cruel." Citing a wellknown

epigram, Mr. Kaminski added, "'The market can stay irrational longer than

you can stay solvent.'"

Nick Amounts, Amaranth's

founder and chief executive, said in August that more than a dozen members of

his risk-management team served as a check on his star gas trader. "What

Brian is really, really good at is taking controlled and measured risk,"

Mr. Maounis said. Mr. Maounis declined to comment yesterday.

When Mr. Hunter began

trading gas eight years ago, it was far less volatile, hovering under $2 a

million BTUs. Mr. Hunter had grown up in farm country near Calgary, but his

knowledge of gas was limited to summer work on a rig in northern Canada. He

knew markets, though: Unable to afford skiing while in college, he poured

himself into math at the University of Alberta. A graduate professor of his was

a leader in the emerging field of financial modeling and derivatives.

Mr. Hunter joined

TransCanada Corp., a Calgary pipeline company that was becoming a player in the

growing business of trading energy, rather than simply transporting it. The company

would help customers like gas producers lock in prices for some of the fuel it

shipped for them.

Mr. Hunter, then 24, came

armed with fresh theories about options pricing and impressed his bosses with

his ability to spot price anomalies. They gave him increasing amounts of money

to trade with after early successes. Among them: He convinced them that options

in Canadian gas were underpriced as a pipeline from Canada to Chicago was set

to open and create a greater market for it.

"He helped us prove

that mathematically...and it paid off hugely," says Shondell Sabad, a

former colleague there who now trades for a Calgary bank.

Traders like Mr. Hunter

make complex wagers on gas at multiple points in the future, betting, say, that

it will be cheap in the summer if there is a lot of supply, but expensive by a

certain point in the winter. Mr. Hunter closely watches how weather affects

prices and whether conditions will lead to more, or less, gas in a finite

number of underground storage caverns. Roughly akin to counting cards in

bridge, a trader keeps track of how much gas is injected into storage and how

much might have been withdrawn for various uses.

Mr. Hunter moved to Wall

Street to do the same work for more pay. He joined Deutsche Bank's energy desk

and gained a name trading U.S. gas futures -- where his wide profit and loss

swings provoked a stormy face-off with superiors.

Mr. Hunter personally

generated $17 million in profit in 2001 and $52 million in 2002, according to a

complaint he later brought in state court in New York. By 2002, he pulled down

more than $1.6 million in salary and bonus and began supervising the gas desk

in 2003.

In December 2003, just as

his group was close to ending the year up $76 million, he claimed in the suit,

things went awry. In a single week, they had losses of $51.2 million, he said

in the suit. He blamed "an unprecedented and unforeseeable run-up in gas

prices" along with "well-documented and widely known problems

with" Deutsche Bank's electronic-trade monitoring and risk-management

software, which he said hurt traders' ability to extricate themselves from bad

trades. Deutsche Bank denied its systems were to blame.

Mr. Hunter argued that

even though the desk as a whole posted a loss, he personally made trades that

netted the bank $40 million that year. He and his natural-gas colleagues got no

bonus. By February 2004, relations had soured to the point that supervisors

locked him out of the trading system and made him an analyst, moving him off

the desk. Mr. Hunter left in April and subsequently sued over the withheld

bonus and claimed Deutsche Bank defamed him. It denied the allegations. The

suit is pending.

Mr. Maounis, the head of

Amaranth, took a chance on Mr. Hunter. Amaranth was one of the first hedge

funds to build an energy desk soon after the demise of Enron, under the

leadership of former Enron energy trader Harry Arora. Messrs. Arora and Maounis

hired Mr. Hunter and initially kept him on a tight leash. Mr. Maounis says the

firm knew of Mr. Hunter's history at Deutsche Bank but did extensive checks and

found "nothing that made us uncomfortable."

Mr. Arora was relatively

conservative and sought to make diversified commodities investments. He brought

Mr. Hunter along and the energy group posted steady annual returns of 20% to

40%.

Mr. Hunter wanted to make

bigger bets in his main market, gas. He had an ability to keep calm with huge

bets on the line and markets were going berserk. In July 2005, for instance, he

was in Calgary at Stampede, a rodeo festival, when the gas market began moving

erratically. Mr. Sabad, his former TransCanada colleague, says Mr. Hunter got

on the phone a few times but didn't panic or trade from his hotel room.

"He asks himself, 'Do I still like my position?' If he does, he adds

more," Mr. Sabad says.

Around that time,

Amaranth agreed Messrs. Hunter and Arora could separate their trading

"books," each controlling his own trades. Then late last year, the

double-whammy of Hurricanes Katrina and Rita made Mr. Hunter a hero at Amaranth

and a minor legend on Wall Street, as he made $1 billion for Amaranth.

Mr. Hunter trolls for

what he calls mispriced options -- that is, the chance to buy or sell something

at a price that appears farfetched to the market but that Mr. Hunter sees as a

distinct possibility. Leading up to the hurricanes, his bets included a complex

portfolio of options based on the idea that gas could get extremely expensive

in the early fall. An option to buy gas at, say, $12 cost very little in summer

2005 because gas was then trading at only $7 to $9. When it surged past $13

after hurricanes ravaged Gulf of Mexico production, such options, which he had

been buying, jumped in value.

His success was a rebuke

to his ex-colleagues at Deutsche Bank, where lawyers were wrangling with him

over his request to take depositions from former superiors, even as he was

banking big profits. It also was hard for Mr. Arora, still his boss but not the

main rainmaker. Mr. Arora eventually left to start his own hedge fund.

It was vindication for

Mr. Hunter. In its annual Christmas card, Amaranth referred to its

energy-market winnings by quoting Benjamin Franklin: "Energy and

persistence alter all things." It sent out toy gasoline pumps.

Amaranth agreed to let

Mr. Hunter trade from his hometown of Calgary, where he began with the fund's

blessings to build an even bigger portfolio. A world away from New York

gridlock, he zoomed to work in his new gray Ferrari, or occasionally a Bentley,

which he tells friends is better in snowy Calgary winters. Besides the cars and

a house he is building, he keeps a low profile. Some of his pickup-basketball

buddies don't even know what he does. Though he consented to several interviews

for this article, he wouldn't allow a photo.

From his desk on a

trading floor, Mr. Hunter monitored dozens of "instant messaging"

tabs from brokers and pored over weather screens. Six traders were there on one

day this summer, in a space crammed with boxes of KitKats and Hershey bars,

microwave popcorn and bags of running clothes. The only fancy touch was a

basketball signed by Michael Jordan encased in Lucite.

'A New Level of Liquidity'

Bruno Stanziale, a former

Deutsche Bank colleague now at Société Générale, works with energy companies

that need to hedge their production. In an interview in July, he contended Mr.

Hunter was helping the market function better and gas producers to finance new

exploration, such as by agreeing to buy the rights to gas for delivery in 2010.

"He's opened a market up and provided a new level of liquidity to all

players," Mr. Staziale said.

Mr. Hunter saw that a

surplus of gas this summer could lead to low prices, but he also made bets that

would pay off if, say, a hurricane or cold winter sharply reduced supplies by

the end of winter. He also was willing to buy gas in even farther-away years,

as part of complex strategies.

Buying what is known as

"winter" gas years into the future is a risky proposition because

that market has many fewer traders than do contracts for months close at hand.

Deals for those far-away months are often done in over-the-counter transactions

that can be hard to exit. In May, his team's position fell nearly $1 billion

when the prices of far-forward gas contracts took a steep dive -- much as they

did last week. In this case, a number of gas producers suddenly sold more gas

than Mr. Hunter expected.

By summer, Mr. Hunter

appeared to be proving doubters wrong. Amaranth's overall fund gained around 6%

in June, was roughly flat in July and rose 6% in August, according to

investors.

Although Mr. Hunter had

fared well, many traders say he was acquiring positions that were too large to

get out of if the market turned -- including a bullish bet on winter gas.

Amaranth won't detail its positions or his trading strategy, so it is unclear

exactly what hurt Mr. Hunter so badly last week. In recent weeks, people

familiar with the transactions say, Amaranth bought MotherRock's gas positions

in an attempt to cancel some of its trades and reduce its market exposure.

Expectations of a

warmer-than-average winter are rising. Last week, the National Oceanic and

Atmospheric Administration said the El Niño weather phenomenon has formed in

the Pacific Ocean. That typically means warmer winters in the U.S. and lessens

the threat from hurricanes in the Gulf of Mexico. All this, and the recent fall

in crude oil, helped to batter gas prices.

Amaranth has scrapped

plans relayed only a month ago to investors to offer them a separate

energy-only portfolio.

Congress, meanwhile, is jumping into the

debate on whether hedge funds exacerbate volatility. The Commodity Futures

Trading Commission argued in a 2005 report that hedge fund trading didn't

increase volatility and even improved the functioning of the markets by giving

energy firms more

No comments:

Post a Comment